Sustainable funds are still working to shake off a difficult spell, as investors prioritising environmental, social and governance (ESG) themes struggle against politicisation and a wider focus on more immediate geopolitical tensions and economic strain.

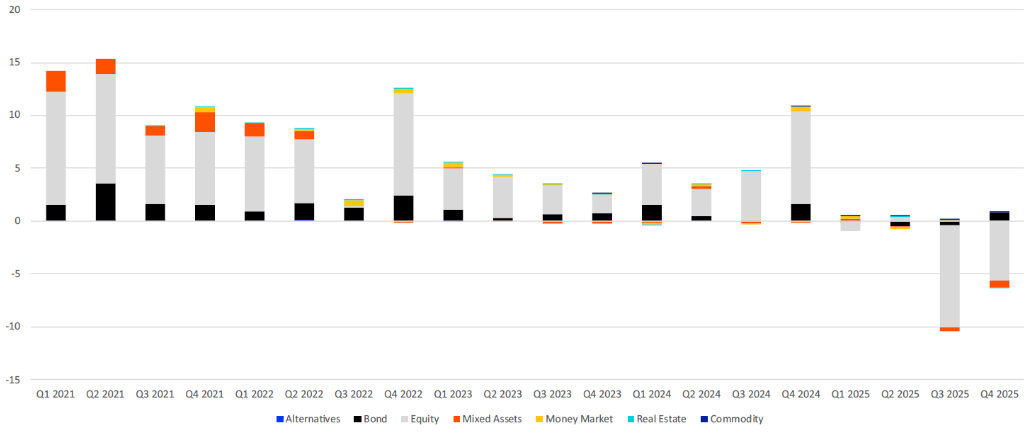

According to LSEG Lipper data, sustainable funds logged four consecutive quarters of outflows in 2025, with sustainable equity funds the biggest contributors to redemptions.

Quarterly flows of sustainable funds over 5yrs (£bn)

Source: LSEG Lipper

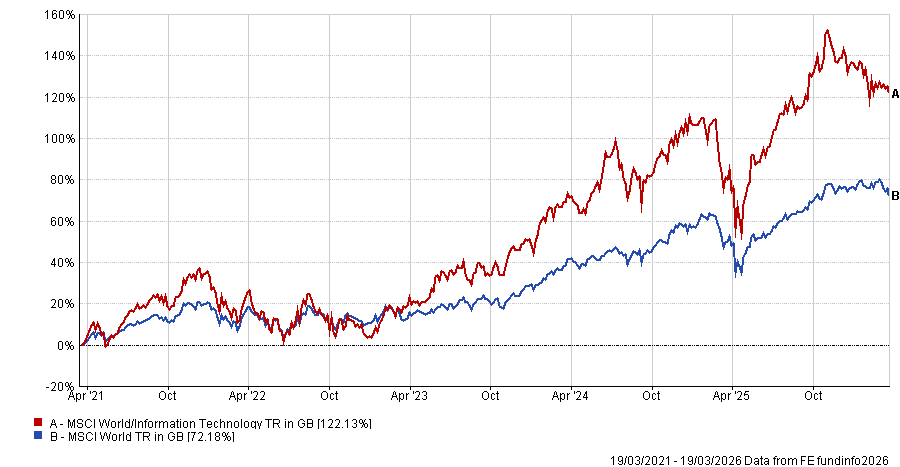

Despite weakened appetite, many sustainable investment strategies have maintained competitive returns.

This resilience has been underpinned by a long-standing overweight to technology stocks historically seen as low-carbon, high-growth drivers of performance.

The MSCI World Information Technology index posted a 122.7% five-year return to February 2026, compared to the MSCI World’s 87.1%.

Performance of MSCI World Information Technology vs MSCI World over 5yrs

Source: FE Analytics

Tech dominance has intensified with the AI boom, with the indexes shown in the graph above diverging from 2023 as large-scale investment began – marked by the launch of ChatGPT.

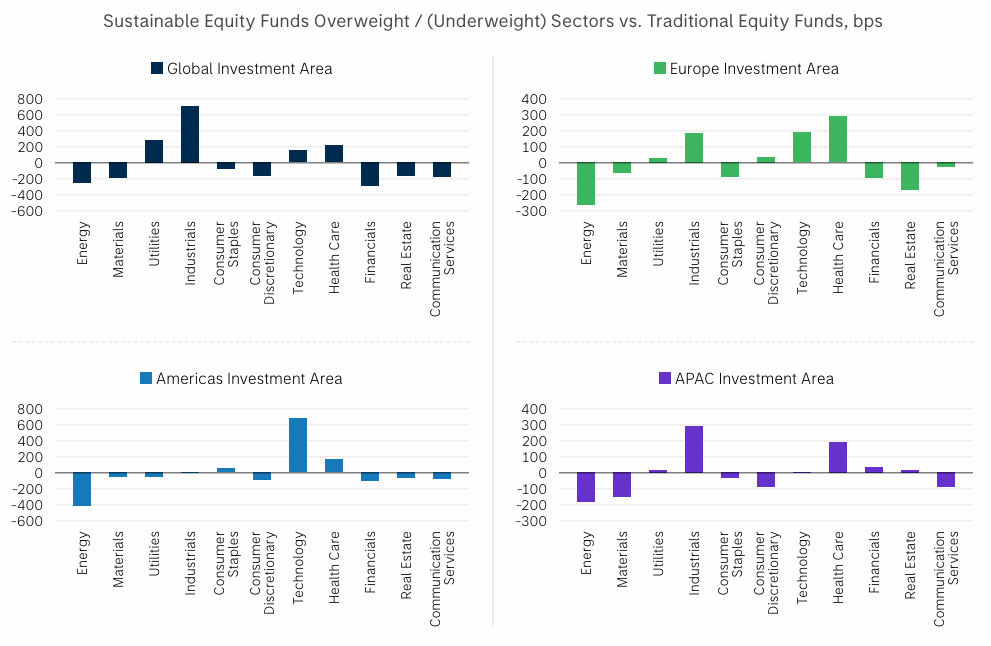

A 2023 report published by Morgan Stanley noted that, at the time of the tech boom, sustainable funds targeting the Americas were overweight technology and more likely to outperform, holding an average 29% of assets in technology versus 23% for equity funds generally, although this was not the only factor influencing outperformance.

Sustainable fund sector weightings in early 2024 (bps)

Source: Morgan Stanley Institute for Sustainable Investing, Morningstar. Data as at 9 February 2024.

According to more recent data analysis provided to Trustnet by MainStreet Partners, across 398 assessed sustainable funds, the median tech allocation is around 25% today.

Sophie Meatyard, head of funds research at MainStreet Partners, said: “Roughly three in 10 funds hold 30% or more in tech and around 8% hold over 40%.”

A minority are deliberately avoiding the sector, with just over 20 of the assessed funds reporting zero exposure to tech, she said.

But the rapid growth of AI is now introducing more ESG-related risks into sustainable portfolios, with problems ranging from heightened carbon emissions and energy usage, to water stress, supply chain transparency and use of AI in weapons and surveillance. As a result, the sector could be becoming less green than it once seemed.

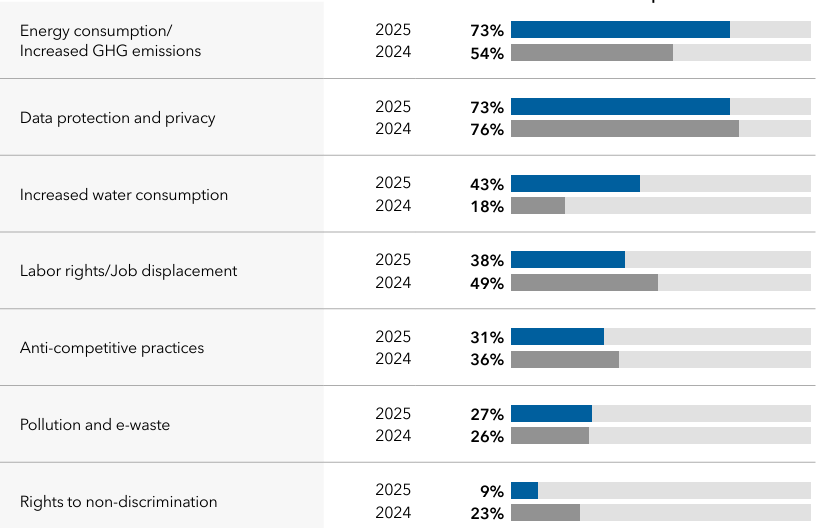

A 2025 survey published by Capital Group found that the majority of more than 1,000 investor respondents were concerned about the energy intensity and potential invasiveness of AI. The former logged the biggest increase in concern over one year.

Most material AI-related ESG investment risks in the near-term

Source: Capital Group

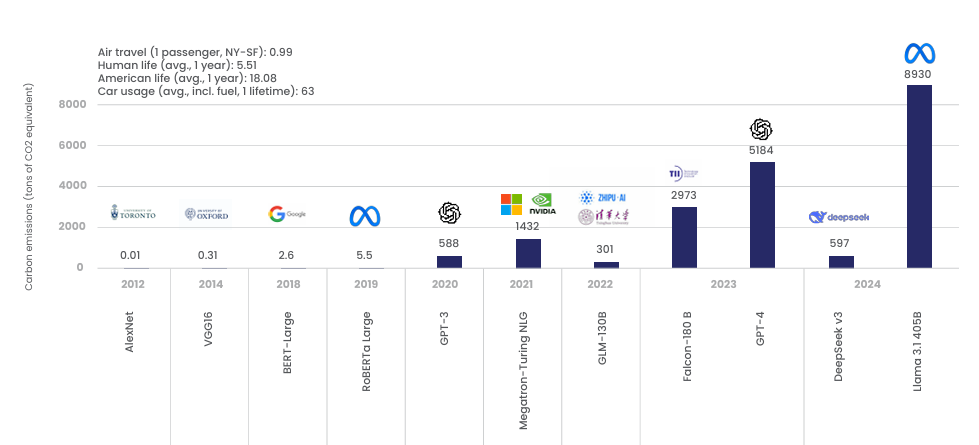

The huge amount of power required to train ever-larger AI models has become clearer over recent months, with resulting emissions shaped primarily by model size, data centre efficiency and the carbon intensity of the electricity grid.

Estimated carbon emissions from training select AI models and real-life activities, 2012-2024

Source: Candriam, Stanford University

Water usage is another environmental risk to consider, as AI data centres require significant amounts of water for cooling purposes, increasing water scarcity in the surrounding area.

A 2025 report from the UK’s Government Digital Sustainability Alliance noted that AI is predicted to lead to an increase in global water usage from over 1 billion to 6.6 billion cubic metres by 2027.

Meanwhile, the International AI Safety Report 2026 mapped the growing range of social risks, from malicious misuse of generative tools for scams, fraud and non-consensual imagery, to more subtle forms of influence as AI-generated content increasingly matches human persuasion. It noted there is also emerging evidence showing criminal groups using AI to aid cyber-attacks.

At a societal level, the report said AI threatens to reshape labour markets by automating cognitive tasks and reducing opportunities for early-career workers, while widespread reliance on AI tools may erode critical thinking, deepen automation bias and, in some cases, contribute to loneliness and reduced social engagement.

With all of this in mind, fund managers are increasingly having to consider whether tech stocks – and which ones – have a place in their portfolios, while investors must be more diligent on whether their funds are investing in-line with their own morals.

How institutional investors view technology and sustainability

Technology concentration is not lost on asset owners. Patrick O’Hara, head of responsible investment and stewardship at LGPS Central – which is responsible for over £90bn in assets of local government pension scheme (LGPS) funds across the UK – said: “There is a bit of a tech problem in sustainable funds.”

LGPS Central invests through segregated mandates, setting restrictions and areas of focus for the managers it works with.

“Because of that, many of our sustainability strategies are not top-heavy in large-cap tech,” he said, pointing to the growing environmental and social risks associated with the sector.

Many other asset owners feel the same. Tom Attwoll, senior specialist in investment practices at the UN-convened Principles for Responsible Investment (PRI) – a body helping asset owners and managers integrate ESG factors into investment decisions and ownership practices – said there is increasing interest from asset owners about the ESG-related risks of the technology sector.

“For many, these considerations are tied directly to long-term value creation and risk management responsibilities,” Attwoll said. These expectations often filter down to the asset managers that asset owners work with.

LGPS Central has quarterly meetings with fixed income managers and annual meetings with equity managers challenging them on portfolio construction, ESG rationale and engagement outcomes.

These conversations have, at times, led managers to avoid or divest certain holdings where engagement was unlikely to deliver change, according to O’Hara.

“Our influence is soft, but managers know we will scrutinise them – we monitor closely, as the proof of the pudding is in the eating,” he said.

Although he has concerns regarding the dominance of tech stocks in sustainable funds, O’Hara also stressed that the picture is far from black and white.

He argued there is a risk of ESG assessments becoming overly reductive if asset owners and managers are not willing to grapple with the full complexity of technology’s impact – both positive and negative.

For example, on the positive side, he noted how AI is increasingly being used to map climate patterns or contribute to healthcare innovation.

“Asset managers may need to communicate risks, opportunities and positive impacts more clearly and holistically to asset owners [and other investors],” O’Hara said.

“We also need to embrace that nuance when analysing portfolios. That doesn’t mean greenwashing – it means having a rounded conversation.”

This is part one of a two-part series. Part two can be found here.